Reimagine growth at Elevate – Dallas 2025. See the Agenda.

Filter

Displaying 31-40 of 143

Continuous Modernization in an Era of Cost Efficiency: Perspectives for BFS Firms in APAC | Webinar

On-demand Webinar

1 hour

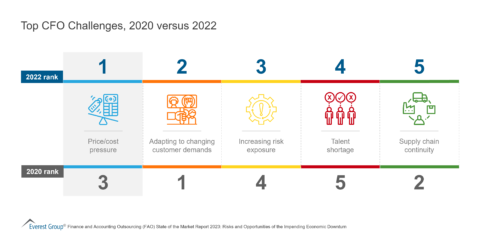

Top CFO Challenges, 2020 versus 2022 | Market Insights™

by Shirley Hung

and 4 others

by Shirley Hung

and 4 others