Reimagine growth at Elevate – Dallas 2025. See the Agenda.

Who We Serve

We strengthen bold leaders – from the world’s largest companies to ambitious disruptors – helping them outpace the competition and shape the future.

What We Offer

Our memberships, custom support, and in-depth published research equip you with the reliable information you need to make data-led decisions with measurable success.

Our Expertise

We blend deep industry expertise with leading-edge research driving growth, innovation, and resilience. With Everest Group, data meets strategy, and vision turns into measurable impact.

Insights

Our wealth of resources inspires ideas and new ways of thinking with real-world solutions and the latest trends that drive your business forward.

Company

We’re committed to helping you get it right. Through trusted expertise, rigorous research, and practical insights, we enable businesses to make confident decisions.

Filter

Displaying 21-30 of 460

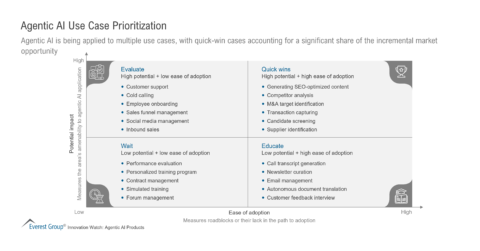

Agentic AI Use Case Prioritization | Market Insights™

Harnessing Digital Workplace Investments for 2025 | Webinar

On-Demand Webinar

1 hour

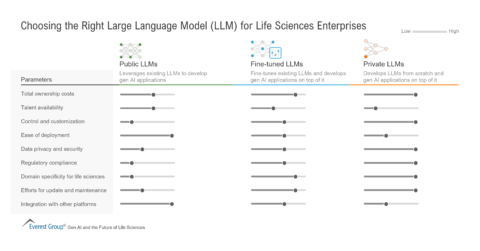

Choosing the Right Large Language Model (LLM) for Life Sciences Enterprises | Market Insights™

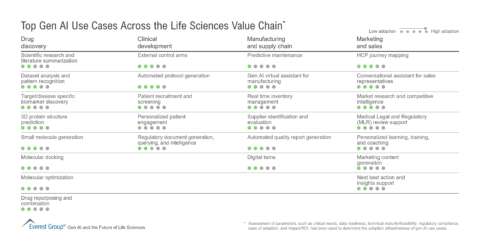

Top Gen AI Use Cases Across the Life Sciences Value Chain | Market Insights™

Global In-house Center (GIC) Setup Capabilities in India – Provider PEAK Matrix® Assessment

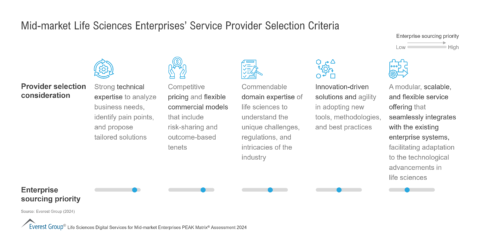

Mid-market Life Sciences Enterprises’ Service Provider Selection Criteria | Market Insights™

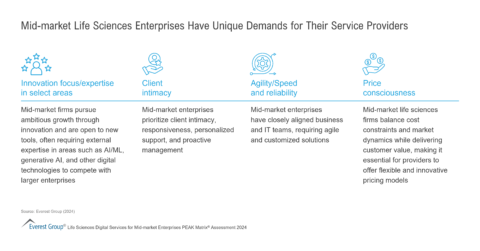

Mid-market Life Sciences Enterprises Have Unique Demands for Their Service Providers | Market Insights™

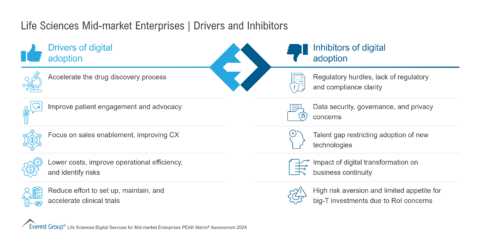

Life Sciences Mid-Market Enterprises – Drivers and Inhibitors | Market Insights™

Will Every Enterprise Platform Become a Data Company? Salesforce Acquires Own Company in a Deal That Will Now Send Ripples Through the Sector | Blog

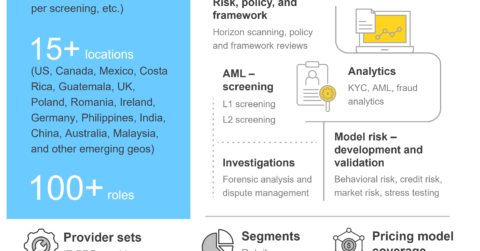

Financial Crime and Compliance (FCC) Services | Market Insights™