Reimagine growth at Elevate – Dallas 2025. See the Agenda.

Filter

Displaying 21-30 of 109

Engineering Services in 2024: The Market Outlook and Commercial Trends | Webinar

On-demand Webinar

1 hour

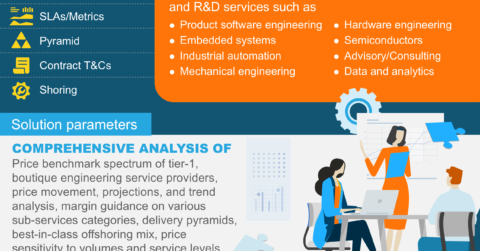

ES Price Benchmarking Catalog 2024 | Market Insights™

by Abhishek Sharma

and 2 others

by Abhishek Sharma

and 2 others