Reimagine growth at Elevate – Dallas 2025. See the Agenda.

Who We Serve

We strengthen bold leaders – from the world’s largest companies to ambitious disruptors – helping them outpace the competition and shape the future.

What We Offer

Our memberships, custom support, and in-depth published research equip you with the reliable information you need to make data-led decisions with measurable success.

Our Expertise

We blend deep industry expertise with leading-edge research driving growth, innovation, and resilience. With Everest Group, data meets strategy, and vision turns into measurable impact.

Insights

Our wealth of resources inspires ideas and new ways of thinking with real-world solutions and the latest trends that drive your business forward.

Company

We’re committed to helping you get it right. Through trusted expertise, rigorous research, and practical insights, we enable businesses to make confident decisions.

Filter

Displaying 1-10 of 71

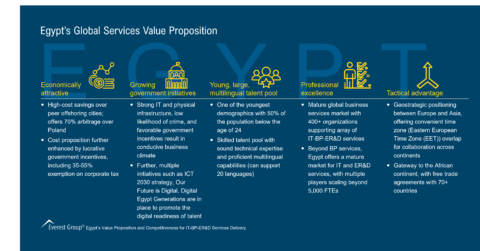

Egypt’s Global Services Value Proposition | Market Insights™

Outsourcing Demand Held Steady in Q4 2021 as Global Sourcing Industry Exhibited Modest Signs of Post-COVID Recovery | Press Release

Retailers’ Evolving Sourcing Strategy Industry | Blog

Outsourcing Demand Falls, Global In-house Center Setups Grow in Q1 2019 According to Everest Group Report on Top Trends in Global Sourcing | Press Release

CRO-to-CRO Video Series: Episode 3 Peels Back the Digital Procurement Platform Onion | In the News

Why is Innovation Important Today? | In the News

Global Sourcing Map 2018 | Market Insights™

The Sourcing Market is on the Up and Up: Everest Group Reports Rise in Global Outsourcing Demand, GIC Activity and Service Provider Revenues in Q2 2018 | Press Release

Global Offshoring and Outsourcing Market—What’s Hot, What’s Not: Everest Group Highlights 2017 Trends, 2018 Predictions in Feb. 15 Webinar | Press Release

Reimagining Global Engineering Services – a Hierarchy of Needs | Sherpas in Blue Shirts