Who We Serve

We strengthen bold leaders – from the world’s largest companies to ambitious disruptors – helping them outpace the competition and shape the future.

What We Offer

Our memberships, custom support, and in-depth published research equip you with the reliable information you need to make data-led decisions with measurable success.

Our Expertise

We blend deep industry expertise with leading-edge research driving growth, innovation, and resilience. With Everest Group, data meets strategy, and vision turns into measurable impact.

Insights

Our wealth of resources inspires ideas and new ways of thinking with real-world solutions and the latest trends that drive your business forward.

Company

We’re committed to helping you get it right. Through trusted expertise, rigorous research, and practical insights, we enable businesses to make confident decisions.

Filter

Displaying 11-20 of 46

Why Less Is More When It Comes to the Future of E-commerce Payments | In the News

The Future of Blockchain in Banking and Financial Services and FinTechs | Blog

Unpacking the Low Code/No Code Opportunity in BFSI | Blog

Delighting Insurance Customers Through a Simplified Experience | Webinar

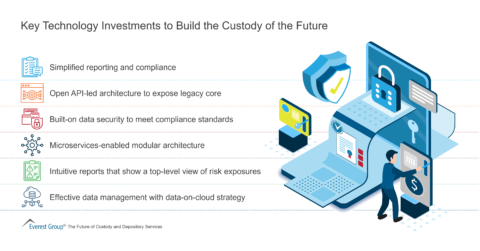

Key Technology Investments to Build the Custody of the Future | Market Insights™

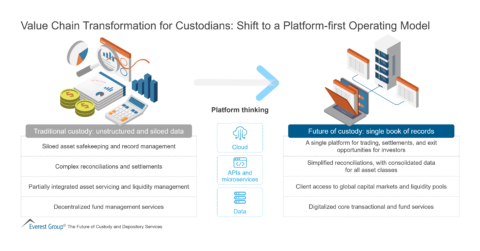

Value Chain Transformation for Custodians: Shift to a Platform-first Operating Model | Market Insights™

A 3-Pronged Approach for Financial Institutions to Accelerate Digital Asset Business | Market Insights™

Simple Platforms for Banking & Financial Services Customers to Manage Digital Assets | Market Insights™

Blockchain Summit India — February 22-23 | Event

FinTech Sandboxes: Good for Business Growth, Good for Countries’ Economies | Blog