Who We Serve

We strengthen bold leaders – from the world’s largest companies to ambitious disruptors – helping them outpace the competition and shape the future.

What We Offer

Our memberships, custom support, and in-depth published research equip you with the reliable information you need to make data-led decisions with measurable success.

Our Expertise

We blend deep industry expertise with leading-edge research driving growth, innovation, and resilience. With Everest Group, data meets strategy, and vision turns into measurable impact.

Insights

Our wealth of resources inspires ideas and new ways of thinking with real-world solutions and the latest trends that drive your business forward.

Company

We’re committed to helping you get it right. Through trusted expertise, rigorous research, and practical insights, we enable businesses to make confident decisions.

Filter

Displaying 41-50 of 50

Enterprise Mobility: Let’s Move BYOnD | Gaining Altitude in the Cloud

Is Mobile Banking the New Banking Reality? | Sherpas in Blue Shirts

Cloud Beyond the Borders – Part 1: Asia | Gaining Altitude in the Cloud

Embrace the Berg: the Real Power Lies Beneath the Surface | Gaining Altitude in the Cloud

Verizon’s Purchase of Advanced Wireless Spectrum | Gaining Altitude in the Cloud

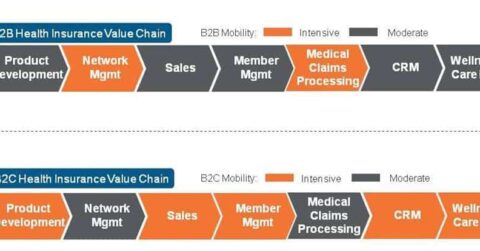

Where Are the Opportunities in Health Insurance Mobility? | Gaining Altitude in the Cloud

If “An Apple a Day Keeps the Doctor Away,” can mHealth Apps Bring Patients and Healthcare Folks Together? | Sherpas in Blue Shirts

The Consumerization of IT may be a Bigger Problem for Business than IT | Gaining Altitude in the Cloud

Live from Bangalore – the NASSCOM IMS Summit, September 21 | Gaining Altitude in the Cloud

Does AT&T Really Need T-Mobile’s Spectrum? | Sherpas in Blue Shirts