Reimagine growth at Elevate – Dallas 2025. See the Agenda.

Who We Serve

We strengthen bold leaders – from the world’s largest companies to ambitious disruptors – helping them outpace the competition and shape the future.

What We Offer

Our memberships, custom support, and in-depth published research equip you with the reliable information you need to make data-led decisions with measurable success.

Our Expertise

We blend deep industry expertise with leading-edge research driving growth, innovation, and resilience. With Everest Group, data meets strategy, and vision turns into measurable impact.

Insights

Our wealth of resources inspires ideas and new ways of thinking with real-world solutions and the latest trends that drive your business forward.

Company

We’re committed to helping you get it right. Through trusted expertise, rigorous research, and practical insights, we enable businesses to make confident decisions.

Filter

Displaying 31-40 of 69

Global Services and Politics | Sherpas in Blue Shirts

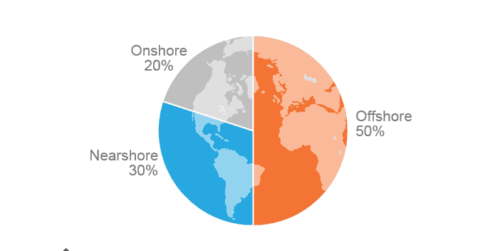

P2P Delivery is Offshore-Centric | Market Insights™

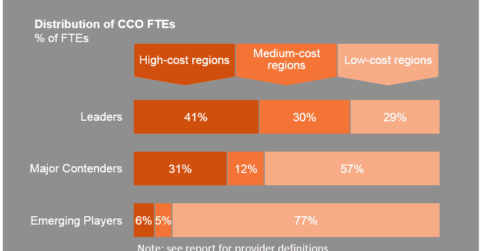

Leading CCO Providers Are Likely to Use A Balanced Delivery Model | Market Insights™

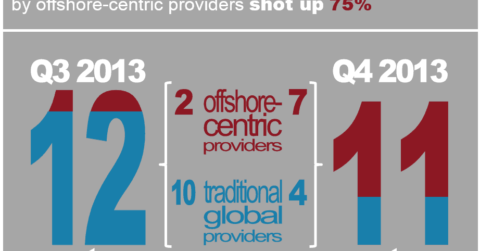

New Provider Locations: Up AND Down in Late 2013 | Market Insights™

The “Prevailing Winds” of FAO Delivery | Market Insights™

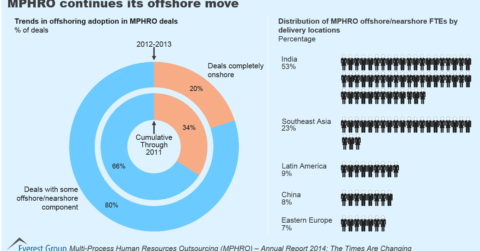

MPHRO Continues Its Offshore Move | Market Insights™

New Players in MSP Accelerating the Move to Offshore Delivery | Market Insights™

Reflections on Impacts on the Global Services Industry in 2013 | Sherpas in Blue Shirts

Malaysia: the Emerging Asian Tiger for Global Shared Services? | Sherpas in Blue Shirts

India’s Tier 2-3 Locations Becoming Hot For Offshore BPO | Sherpas in Blue Shirts