Blog

Deconstructing the Digital Assets Revolution – What Financial Institutions Can Learn from the Meteoric Rise of Coinbase

Digital assets have come a long way from only being Bitcoin to a complete array of increasingly used financial assets. Coinbase’s striking rise has demonstrated a growing acceptance for cryptocurrency that could stick with traditional investors. Is the future for digital currency real, and what obstacles do banks and financial institutions face to compete in this growing crypto market? Read on to learn more of our insights on the next-generation currency movement.

Growing digital asset options

When Coinbase became the first major cryptocurrency start-up to go public on a U.S. stock market this April, the world started giving crypto more legitimacy and the company’s astronomical valuation has garnered great attention.

Along with the skyrocketing value of cryptocurrencies such as Bitcoins and Ethereum, Coinbase – the preferred platform for U.S. investors to purchase these assets – has grown ninefold over the past year. The investment trend over the past five years suggests that cryptocurrency valuation will cross US$24 trillion by 2027.

This rocketing rise can be attributed to increased interest by retail and institutional investors that started investing in Bitcoins and Altcoins as another option to falling interest rates across the world. Other crypto assets such as Non-Fungible Tokens (NFT) traded nine times in the first half of 2021.

Crypto assets have experienced great growth since their early days. Some of the new types (described below in Exhibit 1 and 2) have unique use cases and designs.

Exhibit 1

Exhibit 2

Investors paying attention

Improved technology and better financial services have fueled a remarkable demand in digital assets, especially by institutional investors, over the past 18 months. Investor groups are getting involved in the market for various reasons, including:

- Retail investors – improved personal finance management, easier payment and remittance services, and increased transparency offered by Distributed Ledger Technology (DLT) through openly verifiable and immutable transaction history databases

- Institutional and High Net Worth (HNW) investors – lower operational costs, high reliability and security, faster transaction processing and almost real-time tracing of contracts and payments, and improved access to liquidity for fundraising

Technology firms partnering

As investor interest grows, several FinTechs and BigTechs are investing in technology and infrastructure to support digital assets. Google has partnered with exchange platforms Paxful and Coinbase to add crypto-based transactions on Google Pay. This also allows users to buy Bitcoins and pay using them. Similarly, leading banking software firms such as Temenos recently partnered with specialist digital asset and blockchain infrastructure player Taurus to help banks bridge the gap between traditional and digital assets.

Early access to data will give FinTechs and BigTechs an edge to better understand investor profiles, investment willingness, and funding goals of a large pool of clients. These larger investor groups are also nimble enough to partner with smaller FinTechs and InsurTechs to provide specialty services through a common digital platform.

Opportunities for banks

Since banks would need to cut through bureaucracy, change management challenges, and garner huge financial resources, it is not likely they will develop these technologies quickly enough for the market’s fast pace. However, we believe that increased participation from traditional financial institutions in managing digital assets will pave the way for digital assets in mainstream banking and payments systems as regulations improve.

Large financial institutions such as BNY Mellon recently invested in building a team of technology and business professionals to develop products and platforms that will allow customers to manage cryptocurrency alongside all their other assets. The custodian also received permission from regulatory bodies to offer crypto custodian services in February 2021.

Similarly, Singapore’s DBS Bank received approval earlier this year from the Monetary Authority of Singapore (MAS) to launch the DBS Digital Exchange for tokenized assets. Global banks such as Deutsche Bank are also building services such as institutional-grade hot and cold storage with insured protection for custody services. Huge potential exists to tap into business segments such as wealth management, estate services, financial planning, and asset services in crypto markets since the current penetration is very low.

To stay ahead of the curve, banks should follow this three-pronged strategy to build, partner, and acquire digital assets skillsets in the market:

- Partner and collaborate: Traditional financial institutions will face several issues in developing

in-house solutions to adopt new financial technologies, such as updating legacy systems and regularly innovating solutions offered to remain competitive in the market and keep up with global regulations. These institutions can partner with FinTechs specializing in developing and servicing such solutions at a global scale in a plug-and-play model - Build and develop: Large financial services firms are developing capabilities and skillsets to stay ahead of the competition in the crypto asset services market. Large Banking and Financial Services (BFS) firms such as Wells Fargo have introduced cryptocurrency funds focused on high net-worth individuals. Similarly, JP Morgan has already tested its stablecoin, JPM Coin, which has been pegged against the U.S. Dollar, and offers a solution to cross-border trade between banks and corporates over blockchain

- Acquire and invest: Financial institutions can nurture and acquire FinTechs start-ups that are aligned with the future of financial technology. They can also directly acquire solutions already developed in the market to enhance their platforms in serving their customers with the latest technologies

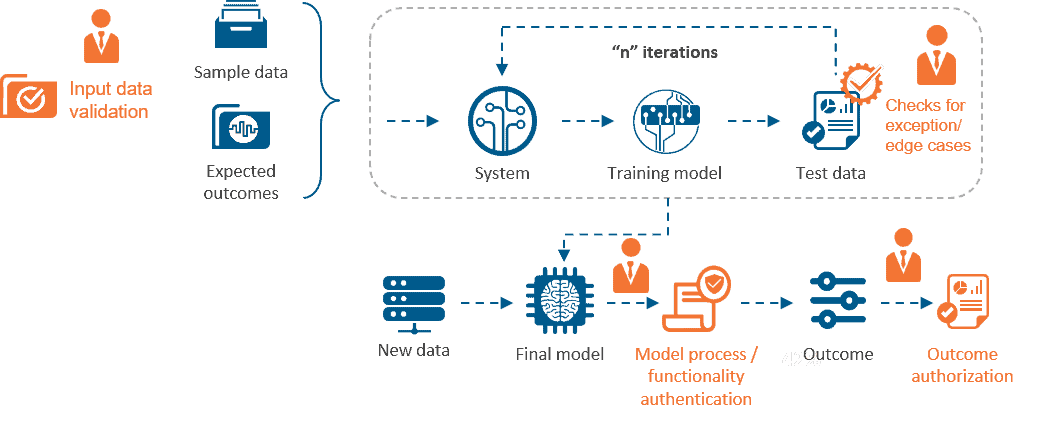

Exhibit 3

Regulatory and other obstacles to overcome

While its potential is promising, banks still face many challenges around regulations, disaster management, private key recovery, insurance-backed custody, and systems for fraud prevention. The biggest roadblock for BFS firms is the lack of clarity of a regulatory framework around digital assets. The process of building a regulatory framework for digital assets will take several years and be iterative. In the interim, policies that are uncertain and not applicable to digital assets should be brought to the notice of regulators and industry bodies as they continuously evaluate policies and provide clarifications.

Banks and financial institutions also will need to make enormous investments in data and technology systems to manage the Risk and Compliance (R&C) around digital assets. Financial institutions will have to adopt a compliance-by-design approach to build platforms to manage the digital assets transactions and the associated mid- and back-office operations. This will require building new data and technology systems for R&C initiatives as no commercially off-the-shelf software in the market has matured enough to manage scaled compliance workflows and operations for digital assets.

For more insights on digital assets adoption, please read our detailed perspective in the report, Deconstructing the Digital Assets Revolution – What Financial Institutions Can Learn from the Meteoric Rise of Coinbase.

If you would like to share your observations or questions on the evolving digital assets landscape, please reach out to [email protected], [email protected], or [email protected].