Blog

Outsourcing “Down Under”: The Impact of a Recession in the Australian Market on Banks

With Australia facing a looming recession, outsourcing is emerging as a solution for banks and financial institutions to navigate economic uncertainty, improve efficiency, and find expert talent. Read on to learn more about the impact of an Australian recession on the industry and opportunities for service providers.

The Australian market is not immune to a recession

While the Australian economy has avoided a recession for the past 27 years, it may not be able to withstand the current environment. Its long history of stability can be attributed to relatively stronger population growth than other developed countries, with Australia recording an average 1.37% growth rate between 1992-2017. Clear-eyed decisions by the Reserve Bank of Australia (RBA) on when to follow the US on rates, plus a large reserve and export of minerals and other natural resources, also contributed to Australia ducking a few recessions.

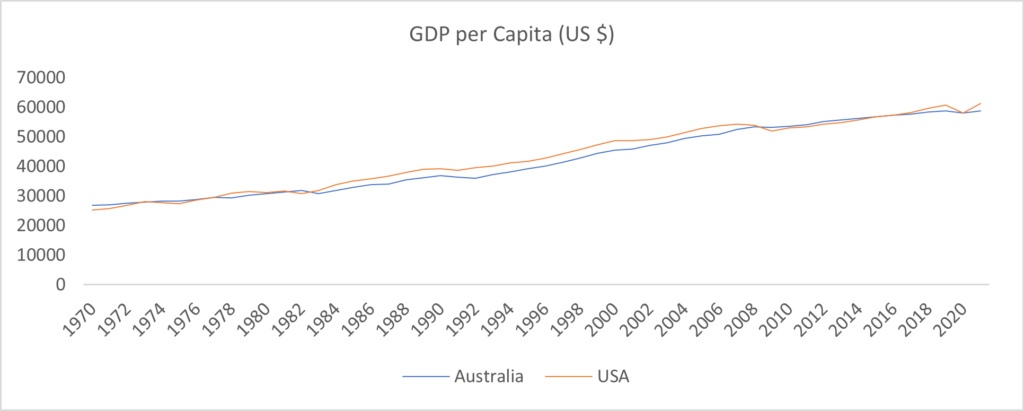

But comparing the Gross Domestic Product (GDP) per capita for the US and Australia from 1970-2021 shows a similar pattern that could signal an economic slump.

Although the American reaction to financial crises seems exaggerated compared to the Australian market, the direction is very similar, with a strong correlation coefficient of around 99% and a coefficient of determination of around 98%.

Correlation doesn’t imply causation, but we can reasonably infer that they tend to move in similar directions or at least are impacted by similar global trends, showing that Australia isn’t as shielded from the global recession as the world wants it to be, at least at a per capita level.

Key drivers for the slump

The Australian recession (at least in per capita terms) is slightly complex. Unlike other countries globally, one key driver isn’t behind the economic downturn. Instead, the following hindrances are impacting its economy to varying degrees:

- Higher energy costs – Supply-side energy price inflation has a greater impact on Australia because of its 71% dependency on fossil fuels. The Consumer Price Index (CPI) rose 1.8 rose in the quarter and 7.3% from the prior year

- Increasing wages – As the labor market tightens, wages increased 2.9% in the private sector in the third quarter of 2022 and 11% from last September. But the increases won’t compensate for rising goods and services prices

- Dropping real estate prices – Even though the number of residential properties rose, the total value fell $359 billion to $9,674 billion this quarter with the average prices falling $36,800 to $889,800

The RBA has been closely observing this situation and is attempting to counter inflation by increasing interest rates, which will lull the economy into a slower state. Interest rates have risen to 3.1% from an almost negligible rate of 0.1% in December 2020. This will greatly hamper consumption and investment spending. Non-discretionary spending increased by 21% in October 2022 from the previous year.

In addition to this, Australian businesses are being marred by the talent crisis, with almost a third (31%) of businesses finding it difficult to find suitable staff and almost half (46%) of businesses experiencing declining operating profits.

Will banks suffer?

In one word: Yes. Financial services have been significantly impacted by the Australian recession. While the Australian banking sector still is dominated by the big four banks (NAB, CBA, Westpac, and ANZ), their share has been declining over recent years with the emergence of tier 2 banks and nonbank financial companies. Operations have been difficult for banks, with almost 20% facing difficulty in finding suitable staff and the cost of doing business rising exponentially.

Rising interest rates also will contribute to lower mortgage originations and refinancing. With consumers having less personal income combined with higher interest costs, residential property investment and mortgage volumes will suffer. Falling property prices also will impact consumer wealth. Apart from originations, financial institutions’ cash inflow will suffer as delinquency rates rise since most loans in the Australian market are variable rate loans.

Also, most transactions now are made using electronic payment methods rather than cash, and checks rarely are used anymore. With the growing trend of using credit cards and increased offerings for buy now, pay later (BNPL), default rates may rise in the future. BNPL also faces challenges under the National Consumer Credit Protection Act, which bans unsolicited credit limit increases and requires background checks for most consumer lending.

Outsourcing as a strategy

Historically, Australia has been an insourced market due to government regulations, job loss concerns, quality issues, and high-profit margins for banks. However, a local talent shortage, high wage inflation, and shrinking profit margins have reversed this trend.

Outsourcing has recently emerged as a popular workforce solution, with 10% of all firms and 22% of large firms considering outsourcing functions in the next three months. This is due to 59% of firms finding applicants’ qualifications insufficient.

Increasing demand for domain-specific expertise, especially in the area of Financial Crime and Compliance (FCC), has made it difficult for firms to find affordable experts. This has led to increased outsourcing interest, even among smaller enterprises. The growing need for technology and expertise in FCC is exemplified by recent cases, such as Westpac’s anti-money laundering (AML) law breaches and the Commonwealth Bank of Australia’s settlement of a $480 million compliance breach case in 2017.

In response to the need for compliance with growing regulations, digital-oriented solutions are in increased demand, and providers are finding success in helping banks improve operations. For example, one bank improved loan origination efficiency by 30% and freed up employee time by transforming its lending operations with the help of Accenture. The National Australia Bank also brought in Accenture to address its financial crimes compliance shortfall and identify high-risk customers.

An effective outsourcing strategy can help banks navigate the current economic recession and achieve cost efficiency with minimal investment and a quick transition time.

How to enter the land down under?

Recognizing that the needs of Australian enterprises differ from those in the US is essential. In this market, digital business process services and digital integration in operations are in growing demand.

However, implementing technology at a surface level will not be effective in Australia, as major banks have previously tried this approach with negative results, making them cautious this time. With stringent regulations, pre-existing products must be modified to meet each financial enterprise’s specific size and sector requirements.

Service providers can utilize their existing global delivery network to gain a foothold in the Australian business process services industry. By offering cutting-edge technology and custom solutions that cater to each client’s unique needs, they can provide more efficient and effective services.

Offshoring can be leveraged for transaction-intensive processes, enhanced with automation and analytics to provide intelligent insights. Modern offerings like business process as a service (BPaaS) can also be utilized, and providers can form partnerships to address gaps in their offerings.

While outsourcing can offer a solution for some functions, critical activities such as payments, mortgage administration, and anti-money laundering (AML), among others, often require complex judgment and technology dependencies and are typically managed by onshore control operations with experience in the Australian market.

To gain additional insights and discuss the impact of the recession on the Australian market and outsourcing’s potential in the Australian banking industry, reach out to [email protected].

Learn about the pricing shifts of outsourcing services caused by the current market in our webinar, Will 2023’s Economic Environment Level Outsourcing Price Increases?