Rising hybrid and multi-cloud adoption, API and machine-identity volumes, and the proliferation of cloud-native architectures have elevated cloud security from an operational necessity to a board-level priority. Beyond traditional configuration management, enterprises must now secure containers, serverless workloads, distributed data stores, and short-lived entitlements – all while addressing AI-driven threats, complex compliance mandates, and rapidly evolving DevSecOps operating models. Enterprises increasingly require a unified approach that delivers real-time visibility, automated guardrails, continuous compliance validation, and contextual threat detection across cloud layers.

Providers are responding with cloud-native application protection platform-driven architectures, automation-first delivery models, and AI-enabled analytics that correlate postures, identities, workloads, and data risks. Providers are also investing in proprietary accelerators, infrastructure-as-code libraries, and co-engineering initiatives with hyperscalers to compress deployment timelines and improve security outcomes. Key priorities include securing AI and generative AI workloads, embedding zero-trust across multi-cloud environments, strengthening cloud-native managed detection and response capabilities, and enabling sovereign-cloud and vertical-specific controls.

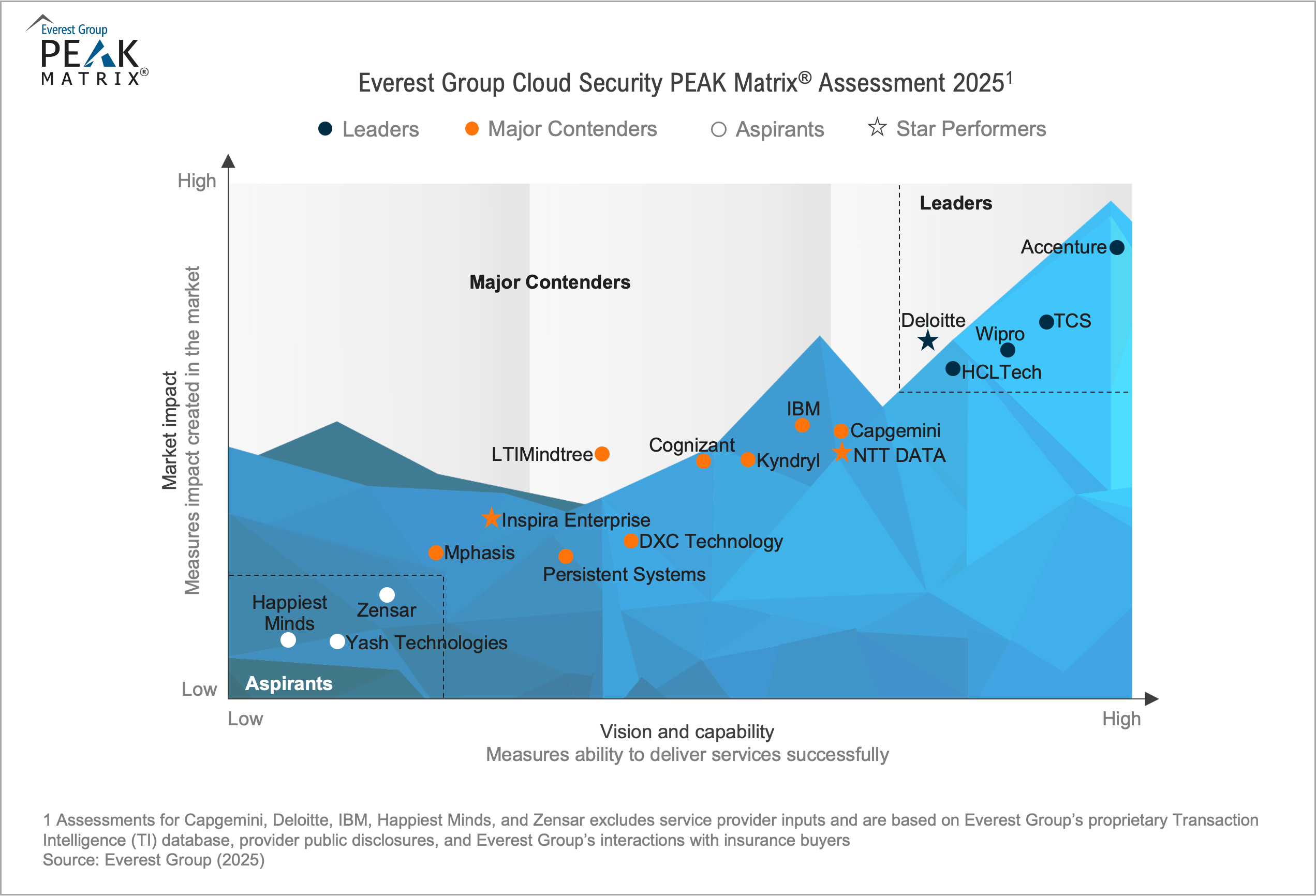

This report analyzes 18 global cloud security providers as featured on the Cloud Security Services PEAK Matrix® Assessment 2025. It enables enterprise buyers to select partners aligned to their cloud-security transformation goals, while providing providers a fact base to benchmark their capabilities.