Blog

The future of FNOL: an agentic front door to claims

The First Notice of Loss (FNOL) is more than just the start of a claim. It’s a strategic inflection point that influences customer trust, operational cost, data integrity, and risk outcomes.

For many insurers, it remains a source of inefficiency, but increasingly it is a major opportunity for transformation. The industry is shifting from manual, disconnected workflows to real-time, data-driven orchestration. FNOL is evolving from reactive reporting to intelligent, proactive triggers via agentic Artificial Intelligence (AI) and connected ecosystems.

This blog views FNOL through three strategic lenses: experience and trust, operational efficiency and automation, and data and risk enablement, mapped across three stages of maturity: Passive, Evolution, and Reinvention.

Reach out to discuss this topic in depth.

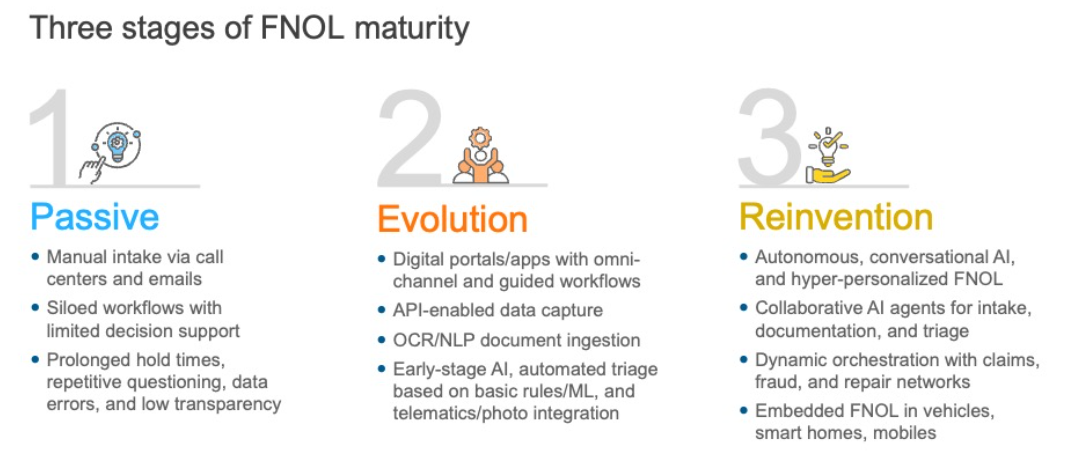

The passive state: Reactive intake and operational silos

In this stage, FNOL relies on manual processes such as phone calls, emails, repetitive data entry, and siloed workflows across departments. Digital channels often replicate these inefficiencies, offering fragmented experiences with limited decision support.

- Experience and trust: According to a survey, nearly 70% of claimants link their claim experience to their initial FNOL interaction. It is often the first post-loss interaction, therefore critical to customer perception. Yet prolonged hold times, repetitive questioning, and lack of transparency persist, leading to dissatisfaction and churn

- Operational efficiency and automation: Manual intake inflates loss adjustment expenses (LAE). It was noted that over 60% of manually filled FNOL forms contained errors or unreadable data, leading to delays and rework. Policy verification and routing consume adjusters’ time that could be better spent managing complexity and service quality

- Data and risk enablement: Though FNOL captures key data, in this stage the data often sits in silos, limiting early fraud detection, reserving, and timely subrogation. Without analytics, insurers lack insight into risk when it matters most

Many small/regional insurers operate in this state, lagging in technology adoption and innovation. Here, FNOL serves as a passive gatekeeper rather than a dynamic catalyst for claims transformation, resulting in friction, cost, and missed opportunities.

The evolution state: Digital foundations with emerging AI capabilities

Driven by shifting customer expectations and connected data sources, many insurers are digitizing intake with intuitive platforms, early-stage AI, and analytics.

- Experience and trust: Omnichannel access via apps, chatbots, voice, and image uploads streamlines the process. Self-service reduces repetitive steps and ensures seamless escalation to human support when needed and real-time notifications provide transparency

- Operational efficiency and automation: FNOL platforms combine photo/video capture and extraction, Intelligent Document Processing (IDP)-driven document ingestion, and Robotic Process Automation (RPA)-enabled data entry/validation with a human-in-the-loop for exceptions, plus light AI-based triage/routing, reducing the average claim creation time to 1 hour compared to the standard 4 to 12 hours in legacy setups

- Data and risk enablement: FNOL becomes a hub for enriched data, integrating telematics, location, and behavioral insights. AI models predict anomalies for fraud detection and guide triage decisions

At this stage, orchestration becomes predictive, supported by supervised AI and ongoing human oversight. But is predictive enough when autonomous is possible?

The reinvention state: Agentic AI powered, autonomous FNOL

The future of FNOL lies in agentic AI, where autonomous digital agents detect, reason, act, collaborate, and learn, with no human input. FNOL no longer just captures incident details but initiates intelligent resolution.

- Experience and trust: Claimants get immediate, empathetic, and personalized responses rather than scripted interactions. Rapid updates and fewer touchpoints reduce frustration and improve satisfaction

- Operational efficiency and automation: Sequential task-handling shifts to event-driven execution. Digital agents manage intake, routing, and document collection at scale, reducing manual burden and shifting adjuster focus to complex tasks

- Data and risk enablement: FNOL data becomes a live asset, powering real-time fraud detection, smart reserve allocation, and proactive loss prevention across the enterprise

Most insurers today operate between the Passive and Evolution stages. The strategic imperative now is to move toward a more advanced state that combines evolution and reinvention stages by using agentic AI, with live proofs emerging: Allianz’s “Project Nemo” uses seven cooperating AI agents (planner, cyber, coverage, weather, fraud, payout, audit) to clear simple NatCat food-spoilage claims via digital FNOL, moving cycle times from days to hours and reporting ~80% faster processing.

AXA Switzerland is an early adopter of Shift Technology’s agentic-AI “Shift Claims” platform that classifies at intake, prioritizes, assists handlers, and automates tasks, reporting a 3% reduction in claims losses, 30% faster handling, 60% automation, and over 99% accuracy in claims assessment. Zurich Insurance also launched a Zurich AI Lab with ETH Zurich’s Agentic Systems Lab and the University of St. Gallen to accelerate research-to-production agentic solutions across claims use cases. Lemonade’s “AI Jim” uses an AI claims bot to clear simple claims through digital FNOL and has demonstrated near-instant settlement, including a 3-second claim payout record. Thus, AI-powered FNOL is not a distant vision but an operational reality for some insurers, delivering measurable improvements in speed, accuracy, and customer satisfaction. So, the key questions are: where does your enterprise sit along this maturity curve, and how ready are you to scale agentic AI?

Why agentic AI?

Compared to generative AI (gen AI) , which primarily reacts to user inputs, agentic AI is more proactive. These agents possess “agency,” enabling them to make independent decisions based on contextual analysis and adapt to changing environments. Agentic AI transforms FNOL from first notice to first action: digital agents plan, act, and adapt in real time, resulting in claims that are faster, more transparent, and customer centric.

- Speed and cost benefits: 24/7 event-driven intake automates data collection, validation, and routing. It handles surge volumes without additional staffing

- Accuracy and consistency: Workflows are standardized and self-learning, reducing errors and rework

- Experience and loyalty: Conversational AI offers clear, contextual, and responsive dialogue, increasing satisfaction and retention

- Risk and actionability: Real-time access to photos, sensors, telematics, and third-party data enables smarter fraud detection, reserve accuracy, and loss prevention

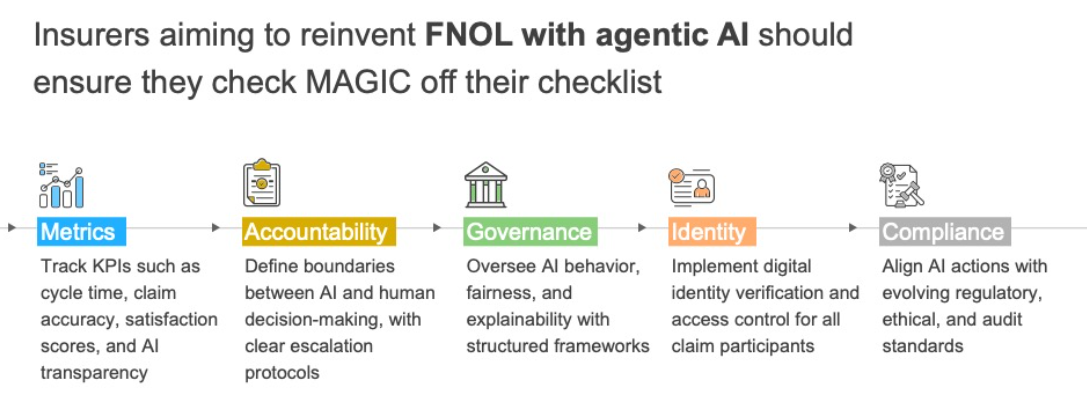

Checklist: Are enterprises future ready?

Achieving agentic FNOL requires more than just technology deployment, it demands readiness across multiple organizational dimensions. To guide this evolution, insurers should evaluate their preparedness.

Only by aligning these five pillars (Metrics, Accountability, Governance, Identity, Compliance) can insurers confidently scale agentic AI from pilots to enterprise-wide impact.

Future FNOL is here, but readiness gaps persist

FNOL is now a strategic component of enterprise transformation, with the potential to drive better outcomes for customers, carriers, and operations. Yet most insurers remain between passive and evolving stages. Only 7% of insurers have successfully brought their AI systems to scale, that is, few have installed even the most effective solutions beyond pilot-level. The question is not whether FNOL will be reinvented, but how quickly. Insurers that act now will be the ones to shape the future of claims.

Everest Group partners with insurers and service providers to benchmark FNOL digital and AI maturity, design Request for Proposals (RFPs) and identify transformation levers, and build pragmatic roadmaps for agentic FNOL adoption and integration.

If you enjoyed this blog, check out, Insuring the future: The Dawn of Smart Insurance in the ACES Mobility Era – Everest Group Research Portal, which delves deeper into another topic relating to insurance and FNOL.

Contact Abhimanyu Awasthi ([email protected]) and Sakshi Gehlawat ([email protected]) to accelerate your FNOL transformation.