Stablecoins: what comes next as settlement infrastructure moves into the enterprise core

For several years, stablecoins sat at the edge of the market narrative, often treated as crypto plumbing or a trading convenience. That is changing as stablecoins are now being packaged more explicitly as payment, and liquidity infrastructure, with clearer regulatory framing in the US and Europe, and a growing set of mainstream financial and enterprise integrations. For Banking and Financial Services (BFS) enterprises, the shift matters because stablecoins are starting to look less like a crypto product and more like a new settlement layer.

Why does this matter now? Because the market motion is no longer confined to issuers and exchanges. Visa has launched USD Coin (USDC) settlement for US institutions and expanded its work with Bridge on stablecoin-linked cards; Mastercard has rolled out end-to-end stablecoin capabilities and agreed to acquire BVNK; Circle has introduced a payments network for real-time stablecoin settlement; and Swift is building a blockchain-based ledger initiative for regulated tokenized value.

For BFS enterprises, the trigger is practical rather than experimental as stablecoins offer 24/7 settlement, and more programmable money flows at a time when traditional rails still impose cut-off times, and reconciliation friction.

They are unlikely to replace existing rails soon, which means banks and payment providers may need to support a parallel rail and connect it into core payment, ledger, treasury, and compliance systems. That also raises the stakes for core technology providers and service providers , with the opportunity shifting beyond experimentation toward architecture, implementation, control, and ongoing operations.

Reach out to discuss this topic in depth.

Why now?

The biggest change is institutional packaging. In the US, the Guiding and Establishing National Innovation for US Stablecoins (GENIUS) Act created a federal framework for payment stablecoins, including reserve, disclosure, and compliance expectations, and the Office of the Comptroller of the Currency (OCC) has already proposed implementing regulations for issuers under its jurisdiction.

In Europe, the Markets in Crypto-Assets Regulation (MiCA) has established uniform market rules for crypto-assets, while the European Securities and Markets Authority (ESMA) has pushed providers to align services with MiCA requirements. That does not remove risk, but it lowers the barrier for banks, payment providers, and enterprise teams to move from pilot conversations to operating-model decisions.

What changes as stablecoins move into payments infrastructure

The infrastructure stack is being assembled end-to-end. At the network layer, Visa and Mastercard are making stablecoin settlement and acceptance part of mainstream payment flows. At the issuer and network layer, Circle Payments Network is designed for banks, payment service providers, virtual asset service providers, and enterprises to move money with 24/7 real-time settlement via stablecoins. At the interbank layer, Swift is developing digital-ledger capabilities alongside its existing infrastructure, signaling that tokenized value is becoming part of future payments design rather than a side experiment.

Exhibit 1 highlights how the stablecoin stack is being assembled across network settlement, orchestration, compliance, and enterprise/core integration.

The implication is important. The winning offer will not be stablecoin payments in the abstract. It will be a governed stack that handles access to regulated tokens, liquidity and conversion, wallet and chain orchestration, sanctions and Anti-Money Laundering (AML) controls, reconciliation, and seamless handoff into payment, treasury, and Enterprise Resource Planning (ERP) workflows. In that model, value shifts away from the token itself and toward orchestration, integration, and risk control. That is exactly where infrastructure players are concentrating their product design.

Enterprises are starting with practical use cases

Enterprise adoption is also getting more pragmatic. Stripe now supports stablecoin acceptance and payouts and has used Bridge to launch Open Issuance, which lets businesses launch and manage their own stablecoins. Shopify has partnered with Coinbase and Stripe to bring USDC payments to merchants. Within BFS, the signal is also strengthening with Cross River Bank and Lead Bank have already started settling with Visa in USDC. That makes these payments and treasury conversation for BFS enterprises, not just a crypto-adjacent one.

That pattern matters because enterprises are not waiting for a wholesale replacement of traditional rails. They are inserting stablecoins first where the pain is highest and the workflow is easiest to measure cross-border payouts, merchant acceptance, treasury mobility, contractor and creator disbursements, and on-chain settlement. BFS enterprises and service providers should read that signal carefully. Initial demand is likely to center on narrow, outcome-led deployments, not enterprise-wide transformation programs.

Core technology is moving closer to the rail

Core technology providers are moving quickly because stablecoins only become operationally useful when they connect to the systems enterprises already run. SAP Digital Currency Hub connects core ERP processes to blockchain-based stablecoin payment rails and supports ISO 20022-based account statements. FIS is integrating Circle functionality into its Money Movement Hub. Finastra is working with Circle to bring USDC settlement into bank cross-border payment flows. These are not side experiments; they are attempts to wire stablecoin capability into existing operational systems.

At the same time, providers are going beyond enablement into productization. Fiserv is positioning FIUSD as a stablecoin that fits into existing banking and payment systems. Oracle’s Digital Assets Data Nexus is designed to help financial institutions launch and govern digital assets with multi-ledger infrastructure, orchestration, security, and compliance capabilities. The strategic signal is clear: Stablecoins are moving into the financial core, not remaining in an adjacent innovation lab.

Exhibit 2 illustrates how competitors are moving by layer: networks, orchestration and issuance platforms, enterprise payment platforms, and core technology vendors.

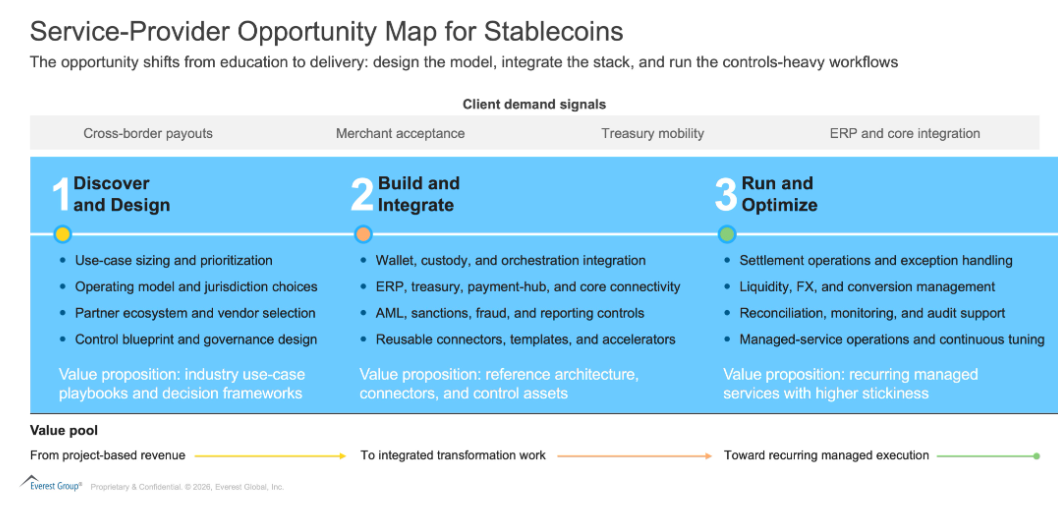

What this means for service providers

What this means for service providers

For service providers, this creates a clear opportunity map. The first offer is strategy and operating-model design: where stablecoins fit versus other emerging money formats, which use cases are viable, and which partners and jurisdictions make sense first. The second is build-and-integrate: wallet architecture, custody choices, payment hub connectivity, ERP and treasury integration, ISO 20022 mapping, and controls for AML, sanctions, fraud, dispute handling, and reconciliation. The third is run-and-optimize: liquidity operations, exception handling, reporting, and managed services.

Competitor activity also indicates where not to play. Networks and software platforms are already productizing settlement and merchant flows. Infrastructure firms such as Bridge, Circle, Fireblocks, Coinbase, and BVNK are abstracting issuance, orchestration, and compliance complexity into Application Programming Interfaces (APIs) and platforms. Core vendors are embedding stablecoin rails into bank and enterprise systems. That means service providers that stay at the level of thought leadership or policy interpretation will get squeezed from both sides.

The stronger position is to become the translation layer between business outcomes and new payment infrastructure. That means industry-specific blueprints, reusable accelerators, ecosystem partnerships, reference architectures, and governance models that help clients move from curiosity to production safely. In stablecoins, the premium is unlikely to sit with whoever explains the trend best. It will sit with whoever makes the rail usable inside real enterprise and financial workflows.

Exhibit 3 outlines the service-provider opportunity from advisory to build to run, with value concentrating in orchestration, controls, and managed execution.

Stablecoins are now competing less as standalone products and more as embedded infrastructure. The strategic question is no longer whether digital dollars exist. It is who controls the experience, the compliance layer, the integration points, and the economics around them. As networks, platforms, and core vendors move deeper into the stack, service providers still have a meaningful opening, but only if they move now from commentary to capability.

Stablecoins are now competing less as standalone products and more as embedded infrastructure. The strategic question is no longer whether digital dollars exist. It is who controls the experience, the compliance layer, the integration points, and the economics around them. As networks, platforms, and core vendors move deeper into the stack, service providers still have a meaningful opening, but only if they move now from commentary to capability.

If you enjoyed this blog, check out, Stablecoins Go Mainstream: How Enterprises, Tech Firms, and Regulators Should Respond – Everest Group Research Portal, which delves deeper into another topic relating to stablecoins.

Reach out to Ronak Doshi ([email protected]), Kriti Gupta ([email protected]), and Laqshay Gupta ([email protected]), to discuss this topic in depth.