Blog

P&C insurance TPAs in North America: market reality, emerging risks, and what comes next

Third-party Administrators (TPAs) have become essential partners in the North American Property and Casualty (P&C) insurance ecosystem. Once treated as transactional vendors for low-complexity or overflow work, TPAs today underpin critical parts of the claims value chain, providing talent capacity, digital capabilities, regulatory fluency, and operational flexibility that insurers increasingly struggle to build in-house.

Yet TPAs’ expectations are rising just as the market faces macroeconomic, regulatory, and technology disruption. As carriers, Managing General Agents (MGAs), and self-insured entities recalibrate their strategies, TPAs must evolve their own models to stay relevant and competitive.

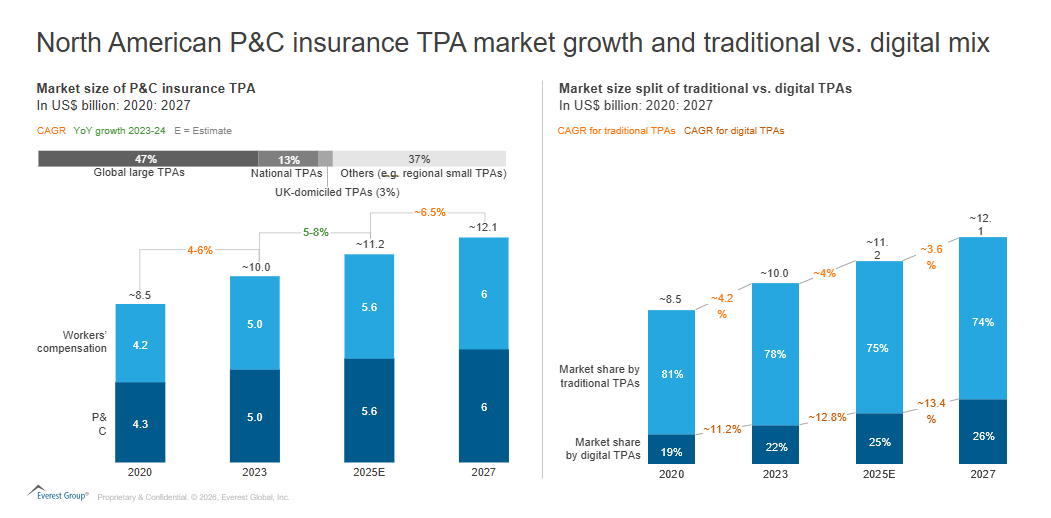

To set the context, Exhibit 1 illustrates the growth trajectory of the North American P&C insurance TPA market and highlights the ongoing shift from traditional, labor-intensive models toward more digitally enabled delivery.

Reach out to discuss this topic in depth.

Exhibit 1: North American P&C insurance TPA market growth and traditional vs. digital mix

The state of the North American P&C insurance TPA market

The P&C insurance TPA market continues to expand, driven by growing claims complexity, rising severity, talent shortages, and regulatory fragmentation. To understand what is driving this demand, Exhibit 2 outlines the core enterprise priorities shaping TPA engagements, highlighting how insurers, MGAs, and self-insured entities increasingly rely on TPAs to balance operational efficiency, regulatory complexity, and rising customer expectations.

Exhibit 2: Enterprise priorities and growth drivers for TPA engagements

Carriers are leaning on TPAs not only for cost and capacity but increasingly for speed, scalability, and digital sophistication.

Several trends are reshaping market dynamics:

- Consolidation and private equity investment are creating scaled, multi-line TPAs capable of offering end-to-end claims solutions. For example, Gallagher Bassett recently announced the acquisition of Reck & Co., a specialist provider of global transport and marine claims services, to expand its claims service offering in Europe

- Digital-native TPAs, though smaller in share, are differentiating through cloud-first architecture, API-driven workflows, and AI-enabled decisioning

- Client expectations are shifting toward transparency, integrated reporting, and experience orchestration across the entire claims life cycle

- Regulatory and cyber pressures are elevating the need for stronger controls, specialized talent, and resilient technology stacks

As a result, TPAs are steadily moving from tactical extensions of carrier operations to strategic partners that influence cost, experience, and risk outcomes.

The pressure points: challenges facing stakeholders across the value chain

Despite market growth, stakeholders face meaningful friction across the TPA value chain.

For carriers

- Fragmented visibility across TPA partners makes it difficult to track performance, leakage, and claimant experience consistently

- Integration challenges with carrier core systems, especially where TPAs operate on legacy claims platforms, slow data exchange and increase manual work

- Escalating severity in auto, liability, and property lines amplifies pressure to manage leakage and accelerate settlements

For TPAs

- Talent scarcity remains acute, particularly in adjusting, clinical case management, litigation support, and SIU roles

- Margin compression continues as clients demand more capabilities without proportional fee increases

- Regulatory and cyber expectations have increased the compliance burden and raised the cost of doing business

- Innovation gaps persist for mid-market TPAs lacking the capital or scale to modernize technology quickly

The net effect is clear: operational complexity is rising faster than traditional TPA operating models can support, accelerating the need for technology-enabled transformation.

Technology as the accelerator: how TPAs are addressing these challenges

The next wave of TPA differentiation will be digital. Leading TPAs are selectively deploying emerging technologies to improve claim outcomes, enhance transparency, and reduce cost.

- AI and advanced analytics

Artificial Intelligence (AI)-powered triage, severity prediction, and subrogation identification are becoming foundational.

Why it matters: Faster routing, better reserving accuracy, and reduced leakage, while enabling human adjusters to focus on high-judgment work. For instance, Sedgwick’s Sidekick/Sidekick+ uses OpenAI GPT-4 via Azure OpenAI to support claims professionals in day-to-day work. Similarly, Gallagher Bassett’s Luminos Claim Summarizer applies generative AI to reduce the need to manually piece together claims narratives

- Internet of Things (IoT), telematics, and connected claims

Sensors, building monitors, and telematics devices are creating new data streams for loss prevention and automated First Notice of Loss (FNOL).

Why it matters: Moves TPAs from reactive handlers to proactive risk partners, especially in commercial property and auto.

- Drones and remote assessments

Drones are accelerating inspections and improving safety during CAT events. For example, Crawford positions WeGoLook as part of its on-demand operating model to support rapid inspection needs.

Why it matters: Reduces cycle times and operational costs while improving accuracy of loss documentation.

- Cloud-based claims platforms and API ecosystems

Modern claims platforms offer flexible, scalable, and integration-ready architectures.

Why it matters: Reduces friction with carrier systems, increases transparency, and enables multi-client, multi-state operations more efficiently.

To bring these technology shifts to life, Exhibit 3 highlights real-world examples of how TPAs are applying digital and AI-enabled capabilities across claims operations, from automation and decision support to clinical case management, demonstrating measurable impact on speed, cost, and service quality.

Exhibit 3: Real-world examples

Across these capabilities, the common denominator is data, the ability to capture it, normalize it, enrich it, and use it to drive decisions. TPAs that industrialize data operations will lead the next phase of differentiation.

The next normal: how TPA business models are evolving

As client expectations shift, so do TPA operating models. Several structural changes are underway:

- Outcome-based pricing

Carriers increasingly expect performance-aligned constructs tied to indemnity outcomes, claimant experience, or cycle time metrics.

TPAs must strengthen analytics and governance to support these models.

- Digital-first operations

Automation, straight-through processing, and AI-assisted adjusting are quickly becoming table stakes.

- Compliance and cybersecurity as differentiators

Auditability, regulatory adaptability, data protection, and cyber posture are now core evaluation criteria, not secondary considerations.

- Ecosystem partnerships

Rather than building everything in-house, TPAs are integrating with InsurTechs, medical networks, restoration providers, and analytics specialists.

- Expansion into emerging lines

Cyber, climate-related losses, parametric products, and complex liability segments are opening new growth arenas.

Taken together, Exhibit 4 illustrates how these shifts are reshaping TPA business models across the value chain, moving from labor-centric execution toward platform-enabled, data-rich operating models.

Exhibit 4: Evolution of TPA models across the value chain

To stay ahead, TPAs must focus on a few decisive priorities:

To stay ahead, TPAs must focus on a few decisive priorities:

- Build differentiated digital capabilities beyond basic automation

- Redesign client engagement around transparency and collaboration

- Industrialize compliance and cybersecurity as competitive advantages

- Monetize data as a strategic asset

- Pursue high-growth niches selectively and strategically

Looking ahead

The North American P&C Insurance TPA market sits at an inflection point. Stakeholder expectations are shifting, operating environments are tightening, and technology is redefining what “good” looks like. TPAs that embrace this moment, by modernizing their digital foundations, rethinking engagement models, and leaning into compliance and ecosystem partnerships, will help lead the next era of claims transformation. Those that do not risk being left behind.

To discuss how the P&C insurance TPA market is shifting, and what it means for your growth strategy, connect with Everest Group. We help TPAs and carriers build resilient, tech-enabled operating models and claims strategies that deliver measurable outcomes.

If you found this blog interesting, check out our research, Subrogation’s Moment to Shine: The Profit Lever Insurance Enterprises Need Now and From defense to intelligence: The future of litigation management in insurance, which delve deeper into key P&C insurance topics.

Please reach out to Abhimanyu Awasthi ([email protected]) or Sohit Kumra ([email protected]).