From controls to intelligent execution: why 2026 is a defining moment for financial crime technology

Financial crime and compliance technology is entering a new phase. For years, institutions addressed regulatory change by adding controls, systems, and manual checks. This response created complex environments that were costly to operate, difficult to tune, and slow to adjust.

Today, expectations are shifting. Regulators want evidence of outcomes, not only evidence of effort. Customers expect protection that does not create friction. Boards want to understand whether investments improve risk, not only increase spend.

Within this context, 2026 is emerging as a pivot point. Regulators want evidence that controls work. Customers want protection without friction. Boards want to see measurable reduction in risk, not just increased spend. Institutions and technology providers are deciding whether to continue adding point solutions or move to intelligent execution systems that act, learn, and explain across the financial crime life cycle.

Reach out to discuss this topic in depth.

From more controls to outcome-driven execution

Traditionally, most financial crime modernization programs have focused on replacing or adding systems. Organizations upgrade case managers, swap screening engines, and deploy new transaction monitoring tools. These changes resolve specific issues but often leave the operating model unchanged.

The next wave focuses on outcomes. Institutions are looking at the quality of decisions, not the number of controls. They want to know how many true risks they identify, how frequently models are recalibrated, how quickly high-risk cases progress, and how consistently human decisions are applied.

This evolution shifts platforms to a system-of-execution model that ingests signals, and orchestrates workflows, applies models, triggers actions, and feeds outcomes into tuning processes. The focus moves from “adding tools” to designing how decisions are made.

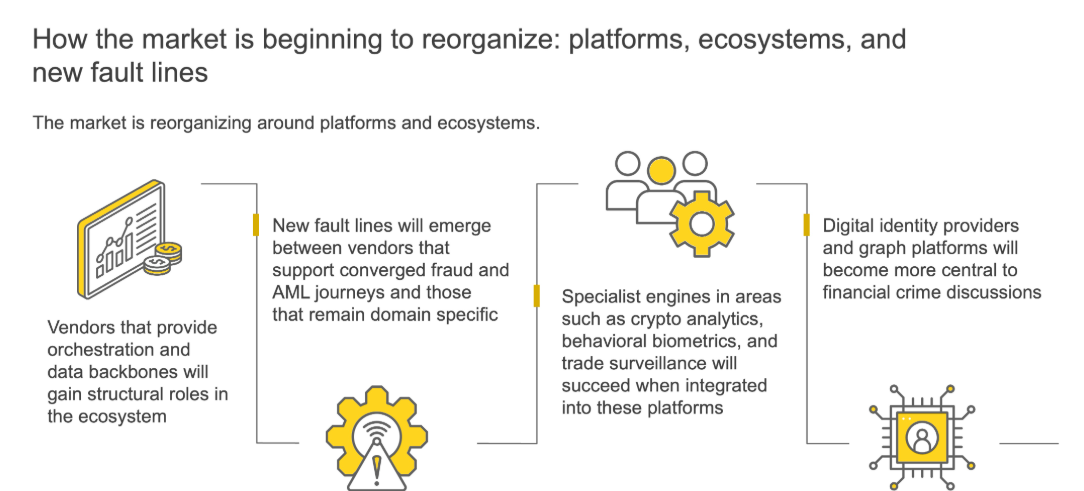

From silos to unified risk fabrics

Many institutions still operate financial crime systems in silos. Know Your Customer (KYC), sanctions, Anti-money Laundering (AML), fraud, and crypto often reside in separate environments with separate teams. Data is copied across systems, sometimes manually, and investigators move across screens to build a customer view.

By 2026, more organizations will progress to unified risk fabrics. These architectures do not require a single underlying engine. Instead, they provide a shared data model, common case record, and an orchestration layer that integrates multiple controls.

Unified risk fabrics allow institutions to ask, “What is the current risk of this customer or network?” and receive one consolidated answer rather than several partial views.

Agentic Artificial Intelligence (AI) and generative AI across the financial crime life cycle

AI capabilities are moving from isolated pilots to embedded functions. Agentic Artificial Intelligence (AI) can perform repeatable tasks such as triaging low-risk alerts, gathering context across systems, and proposing next steps. Generative AI (gen AI) can summarize investigations, draft suspicious activity reports, and explain complex model outputs in business language.

The shift in 2026 is not AI’s existence but the level of trust placed in it to operate within workflows. That trust will rely on traceability, clear role design between humans and machines, and strong model governance.

Real-time and batch layers that work together

Instant payments, real-time account funding, and embedded finance journeys are increasing speed requirements for financial crime controls. Detection cannot occur only overnight. At the same time, some analytical activities, including complex pattern analysis or back-testing, are better suited to near-real-time or periodic processing.

Future architectures will support multiple processing speeds. Real-time layers will screen and score transactions in motion. Near-real-time and batch layers will support deeper analysis and recalibration. Success will depend on treating these layers as complementary, not competing.

Converging fraud, AML, sanctions, and digital asset risk

Criminal activity crosses organizational boundaries. Mule accounts, layered payments, and hybrid schemes that move funds through exchanges or tokens span fraud, AML, and sanctions. Supervisors are also increasing their focus on enterprise-wide financial crime risk.

This is driving institutions toward converged risk views. Investigators will retain specialist skills, but they will increasingly work from shared cases that include fraud indicators, AML patterns, sanctions concerns, and digital asset exposure. Platforms that support convergence will become more central to the financial crime stack.

Digital asset oversight matures

Digital assets are moving from the periphery of financial crime programs to their core. Banks are exploring custody and trading services, and FinTechs are deploying hybrid fiat-and-token models. Regulators are clarifying expectations for virtual asset service providers.

By 2026, on-chain analytics, wallet risk scoring, exchange monitoring, and travel-rule compliance will be standard components of AML and sanctions platforms. The distinction between crypto compliance and banking compliance will begin to narrow.

Digital asset oversight will also influence data strategy as institutions integrate blockchain traces with traditional customer and transaction data.

Regulations as accelerants, not constraints

Regulatory initiatives are increasing urgency. The creation of the European Union (EU) Anti-Money Laundering Authority and related EU rulebooks, coupled with evolving guidance in the United States, signals two expectations. First, supervisors want more consistency and transparency in how institutions design and govern controls. Second, they are increasingly open to advanced technology if it is explainable and well managed.

These developments will accelerate investments in model risk management, explainable AI frameworks, and shared utilities that help institutions demonstrate that their systems work as intended.

Understanding what this shift means

The trends shaping architecture, AI adoption, convergence, and regulation point to deeper changes in how the market is evolving and how institutions will operate.

This dynamic will create opportunity and pressure. Providers that cannot demonstrate how they support unified risk management, rather than individual controls, will find it harder to secure strategic positions.

A defining moment for enterprises and providers

For enterprises, 2026 represents a posture decision. Some institutions will continue to treat financial crime technology as a regulatory cost. Others will view it as a system of execution that protects revenue, builds trust, and enables innovation.

Institutions that hold the latter view will:

- Set clear performance metrics and track them over time

- Invest in architectures that enable reuse of capabilities across products and regions

- Deploy AI where it can responsibly extend human capacity and insight

- Treat digital asset risk as integral to financial crime programs, even with limited current exposure

For vendors, this period will differentiate product suppliers from execution partners. Execution partners will provide domain insight, change support, and roadmaps aligned with regulatory signals such as the EU Anti-Money Laundering Authority (AMLA). They will help clients design operating models, not only deliver features.

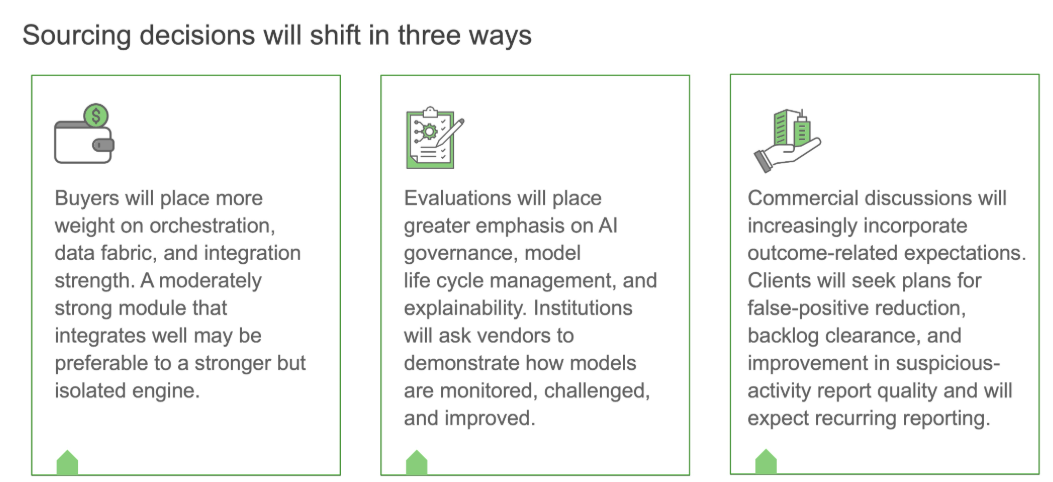

These changes have practical implications. Providers will need to invest in customer success, value engineering, and regulatory engagement. Enterprises will need to adjust sourcing criteria to reflect platform roles, interoperability, and long-term partnership potential.

Turning this moment into long-term advantage

Financial crime technology is shifting from stand-alone controls to intelligent execution across the value chain. Unified risk fabrics, maturing digital asset oversight, and evolving regulatory expectations signal that institutions are expected to understand and manage risk in a more integrated, transparent, and timely manner.

Institutions and vendors that act early will reduce exposure and create conditions for faster product innovation, safer use of AI, and stronger trust with supervisors and customers. This is what makes 2026 a defining moment in terms of not only the technology being deployed but the type of financial crime capability the industry chooses to build.

If you found this blog interesting, check out Compliance singularity: Insights from ACAMS and Sibos on the intersection of regulation, AI, and execution – Everest Group Research Portal, which delves deeper into another topic regarding FCC and regulations.

To take the conversation forward, please contact Rahul Mittal ([email protected]), Kriti Gupta ([email protected]), Ronak Doshi ([email protected]) and Dheeraj Maken ([email protected]).