Blog

How Cost Competitive are Global In-house Centers (GICs)? | Sherpas in Blue Shirts

? | Sherpas in Blue Shirts 1")

Although GICs are an integral component of the global services market with increasing adoption by buyers, there continue to be questions about their cost competitiveness. To obtain the facts, Everest Group conducted GIC cost competitiveness assessments with both source markets (North America and Europe) and service providers. Following are the key findings from our recently released report on the topic.

GICs offer sustainable arbitrage with source markets across locations/functions, and organizations have the potential to increase savings by fully leveraging efficiency levers

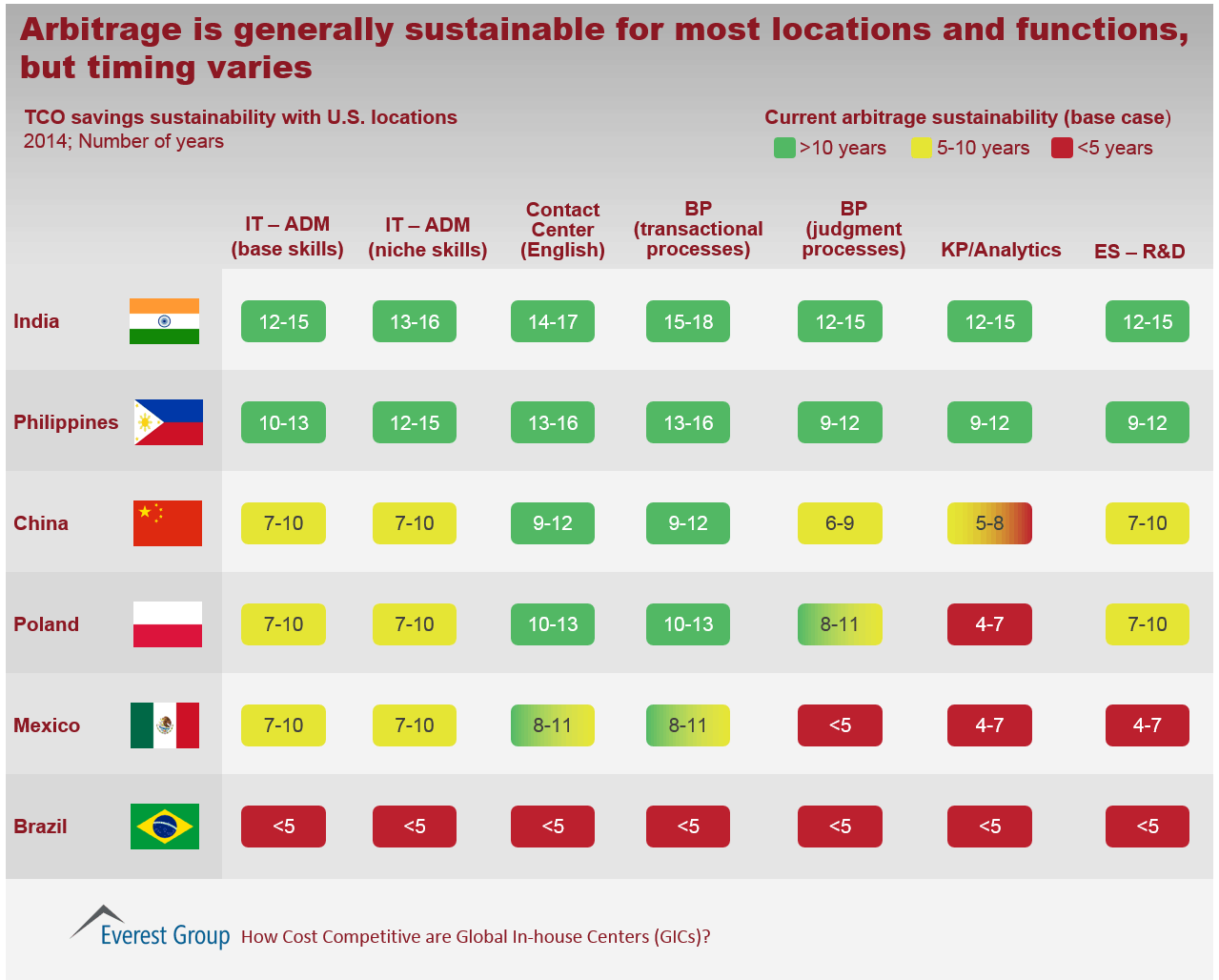

Despite sustainability concerns, our analysis indicates that GICs provide source markets with significant cost savings. Savings typically vary between 30 to 70 percent, across most locations and functions. More interesting is the finding related to change in cost arbitrage across successive years. In India’s case, favorable exchange rates, coupled with a less-than-anticipated impact of wage inflation, has strengthened cost arbitrage over the last two to three years. While the focus in recent years has naturally been on India, it’s important to acknowledge and remember that other leading locations, (i.e., Philippines, China, Mexico, and Poland), also continue to offer similar cost arbitrage compared to the last two to three years.

The report examines the sustainability of cost savings (measured by number of years) in detail by evaluating cost inflation (separate for wages and other cost elements) and forex movements in leading locations. Exhibit 1 provides a synthesized view of our analysis, indicating the sustainability of cost arbitrage for most locations/functions even under aggressive inflation and currency movement scenarios.

Exhibit 1

The sustainability analysis is based on labor arbitrage alone, and excludes the impact of efficiency-based levers such as reducing general and administrative expenses, moving to tier-2 locations, increasing capacity utilization, and increasing span of control and deskilling. While not all GICs have been able to fully leverage and exploit these levers, best-in-class GICs have been able to achieve an additional 10-12 percent savings beyond labor arbitrage.

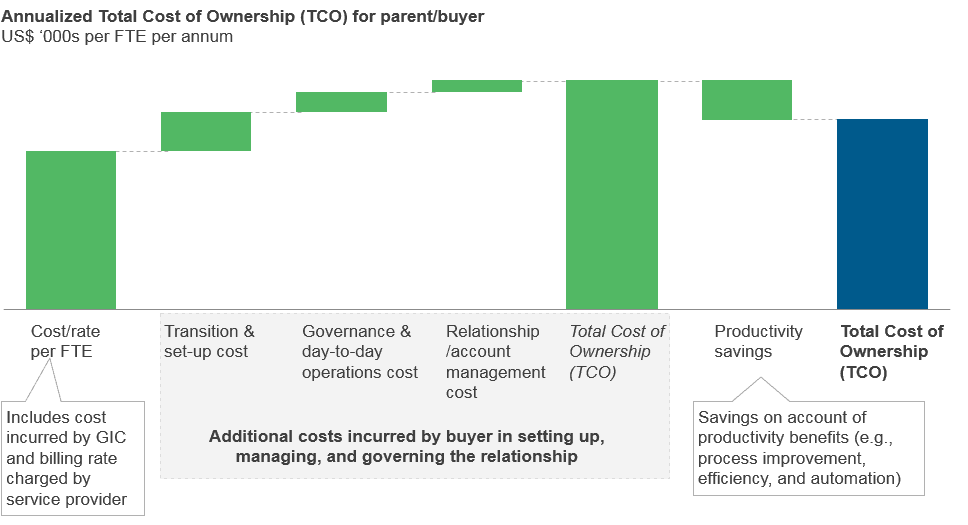

Comparing GIC costs with service provider pricing is too simplistic; organizations need to evaluate the TCO to assess the relative cost difference

In our experience, most buyers compare GIC costs with service provider pricing to assess the relative cost difference between sourcing models. But this comparison often fails to capture the true financial impact of a sourcing decision. Mature buyers evaluate the Total Cost of Ownership (TCO) metric. In addition to hard costs (e.g., salaries, facilities, technology, and telecom), TCO incorporates the soft costs associated with transition, governance, and relationship/account management, along with net impact of productivity measures (see Exhibit 2).

Exhibit 2

Conducting a TCO analysis yields interesting results. Indeed, there are instances in which GICs have significantly lower TCO costs than service providers for certain kinds of work, even though the GICs’ operating costs would be higher than provider rates.

The relative cost competitiveness between sourcing models is dependent on multiple factors. There are those related specifically to the work and where/how it is delivered (e.g., relative scale, process maturity, nature of work, and domain expertise.) There are also company-specific factors driving differences, such as preferences for a more experienced pool, better pedigree talent, market positioning as an employer of choice, promotion of similar organizational culture, and approaches to gain share.

To truly gauge cost competitiveness of GICs with service providers, organizations need to conduct a TCO analysis that takes into account all hard and soft costs and unique requirements.

We are hosting a webinar on Thursday, November 20, that will discuss how GICs add strategic value to the parent organization and how they can quantify that value. Register here.

Photo credit: Tup Wanders