The next battle in revenue orchestration: inside the operating core

The previous blog in this series focused on execution-led orchestrators, providers making revenue orchestration their clearest strategic bet. This blog looks at the same layer from the opposite direction. Enterprise platforms are not trying to build around the commercial stack; they are trying to turn the system of record into an orchestration engine.

That distinction matters because specialists often define a category early, but enterprise platforms often determine how broadly it scales. Systems of record already sit inside the workflows where accounts are managed, approvals are routed, service interactions are logged, and renewals or invoices increasingly sit. As revenue orchestration shifts from insight generation to coordinated action, that control point becomes more strategic. Here, control point means the platform layer that holds the shared customer and commercial context, applies workflow and permission logic, and can trigger or govern actions across teams.

That is why providers such as Salesforce, Microsoft, and HubSpot are broadening their platforms across data, Artificial Intelligence (AI), workflow, service, and monetization. Salesforce is linking Data Cloud, Agentforce, and Revenue Cloud; Microsoft is connecting Dynamics 365, Customer Insights, and Copilot; and HubSpot has expanded Service Hub and Commerce Hub while adding Cacheflow for Configure, Price, Quote (CPQ) and billing. The direction is clear. They are moving closer to the operating core through which revenue activity is governed and executed.

Reach out to discuss this topic in depth.

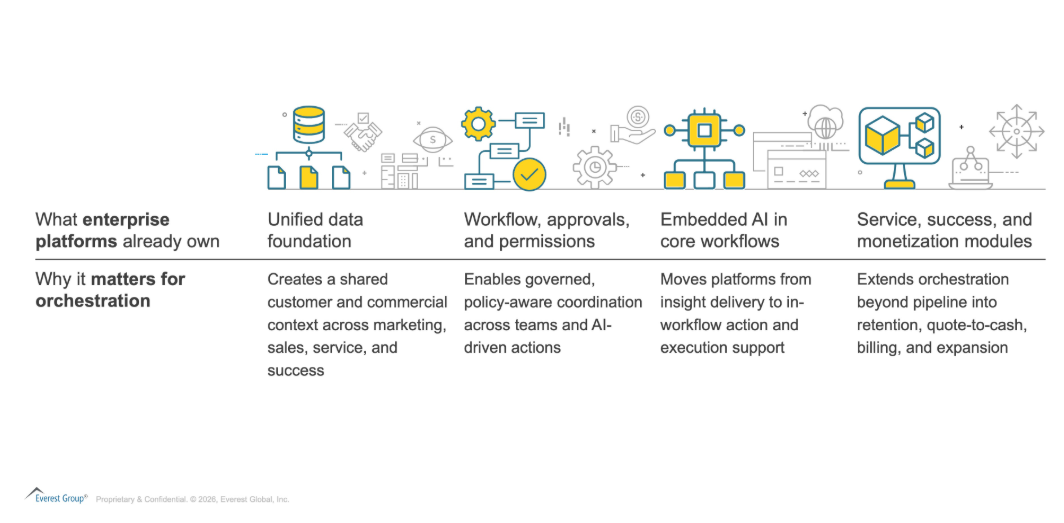

Exhibit 1 sets up the logic behind this shift. It shows why enterprise platforms enter revenue orchestration with a head start; many of the capabilities they already own are increasingly the same capabilities orchestration now requires.

Exhibit 1. Where enterprise platforms have an edge

Reach out to discuss this topic in depth.

Why enterprise platforms are gaining leverage

Revenue orchestration is not just a better dashboard or a cleaner integration layer. It depends on shared objects, common definitions, approval logic, permissions, auditability, and the ability to coordinate action across sales, marketing, service, customer success, and finance. Those are capabilities systems of record already govern.

That matters more now because the orchestration problem is widening. It no longer sits only in lead routing, opportunity management, or sales execution. It increasingly reaches into renewals, billing, quote-to-cash, and post-sales growth. The closer orchestration moves to these governed workflows, the more leverage shifts toward platforms that already manage the commercial core. Specialists will remain relevant where orchestration depends on depth, speed, or domain-specific execution that broad platforms cannot yet match. Specialists can still outperform in focused execution use cases, but enterprise platforms start closer to the operating substrate where cross-functional activity is standardized, controlled, and scaled.

The orchestration layer is moving into the operating core

The orchestration layer is moving into the operating core, driven by three shifts that are redefining platform value:

1. Governed AI is changing the basis of platform trust

As AI moves from recommending actions to taking them, governance becomes part of the product value, not just a support requirement. Salesforce has made trust a design principle through its Trust Layer, which emphasizes grounding in Customer Relationship Management (CRM) data, masking sensitive data, auditability, and zero-data-retention commitments with third-party model providers. Microsoft is making a parallel point through Copilot Studio, where makers and admins get governance controls over access, policies, publishing, and agent behaviors. The message is bigger than either provider: in enterprise orchestration, controllable AI is becoming more valuable than impressive AI.

- Unified data is now table stakes

For system-of-record-led orchestrators, unified data should be viewed less as a differentiating feature and more as a price of entry. Without a common layer spanning marketing, sales, service, and post-sales activity, AI cannot be grounded consistently, workflows cannot be coordinated reliably, and cross-functional handoffs remain fragmented. In that sense, the question is no longer whether platforms need unified data. It is whether they can operationalize that shared context into governed action at scale. That is one reason enterprise platforms are gaining relevance. They already sit closer to the records, permissions, and workflow logic needed to make shared context usable across the revenue life cycle. The advantage, therefore, is not data unification alone. It is the ability to convert that prerequisite into coordinated execution.

- Revenue orchestration is moving closer to monetization

This evolution is where the category becomes materially more strategic. HubSpot is a useful example. In 2024, it launched an all-new Service Hub, expanded Commerce Hub globally, and embedded new AI capabilities across the platform. It later added subscription billing management and CPQ into Commerce Hub. Salesforce’s push with Agentforce for Revenue points in the same direction, orchestration is moving deeper into quote-to-cash and revenue operations, not stopping at pipeline visibility. That matters because retention, billing, pricing, and renewals are where revenue is actually realized and defended. Once orchestration reaches that layer, it stops being just a sales productivity discussion and starts to matter more to commercial and finance leaders as well.

What will separate leaders in revenue orchestration

The category is not moving toward a simple winner-takes-all outcome. Instead, it is becoming a contest over who owns the most credible orchestration control point. That shifts the basis of competition in three important ways:

- The advantage is moving from integration breadth to decision-rights ownership: Historically, platform strength was often measured by how many systems could be connected. Increasingly, the stronger position lies with providers that govern the objects, workflows, approvals, and permissions through which revenue decisions are made and executed

- Proximity to monetization is becoming more strategic: Platforms closer to pricing, billing, renewals, and quote-to-cash have a stronger claim on the revenue control point, as orchestration moves from pipeline visibility to revenue realization

- Execution quality will still separate leaders from followers: Structural control alone will not be enough. Platforms will still need to show that this control translates into better prioritization, faster action, and clearer commercial outcomes. Where they fail to do that, execution-led specialists will continue to retain an advantage

This dynamic is the key market tension. Enterprise platforms now have a credible path to absorbing more of the orchestration layer, but leadership will not be decided by platform breadth alone. It will depend on which providers can turn ownership of the operating core into better revenue execution.

The next phase will be decided in execution

The deeper implication is not that the system of record automatically wins. It is that more of the value in revenue orchestration may migrate toward platforms that already own the commercial core. In larger enterprises especially, that makes the system-of-record-led model increasingly plausible.

However, the bar is rising. Platforms that stop at governance, broad workflow coverage, and data unification will still leave room for specialists. The next phase will be shaped by providers that can turn structural control into measurable commercial execution across the buyer life cycle.

The system of record, in other words, is no longer being judged only on its ability to store activity. It is increasingly being judged on its ability to direct it. And that is what makes the battle for the revenue control point one of the clearest signals in where revenue orchestration goes next.

The next blog in this series will examine the third archetype, signal-led platforms, and how the ownership of conversational, behavioural, and success signals creates a different route into the orchestration layer.

If you enjoyed this blog, check out, The structural choice for CXM GCCs – Everest Group Research Portal which delves deeper into another topic relating to topics mentioned in this feature.

If you would like to discuss revenue orchestration platforms in more detail, please reach out to David Rickard ([email protected]), Divya Baweja ([email protected]), or Rakshit Hooda ([email protected]).