Blog

The cycle to get right: Five priorities for critical minerals R&D leaders in 2026

Reading the 2026 price action and capital movement

A 557% tungsten move and a 30% praseodymium-neodymium move are the same story, told twice. Ammonium paratungstate (APT) prices on the Fastmarkets European benchmark rose 557% after China’s February 2025 export controls, hitting US$2,250 per metric ton unit by March 2026 [1].

Praseodymium-neodymium oxide on the other hand, rose 30% in the first quarter of 2026, as Chinese export licensing tightened, with European prices at six times Chinese domestic levels [2][3]. Lithium proves the point by reversal: prices stayed soft after an 80% collapse following 2023 [4]. The strategic bottleneck has moved to midstream processing and qualified output.

However, capital is mobilizing differently. The capital response is unprecedented in size and structure. US federal commitments topped US$30 billion into the February 2026 Critical Minerals Ministerial: Project Vault, a US$10 billion Export-Import Bank loan plus US$2 billion private capital [5]; a US$600 million Development Finance Corporation (DFC) stake in the US$1.8 billion Orion Critical Mineral Consortium [6]; a US$5 billion DFC equity revolving fund from the Fiscal Year 2026 National Defense Authorization Act, with minority equity authority raised to 40% [7].

Canada added a US$2 billion Critical Minerals Sovereign Fund with US$12.1 billion in allied partnerships [8]. The World Economic Forum and Columbia SIPA noted in May 2026 that investability is the binding constraint: long timelines, permitting complexity, weak revenue visibility, and policy uncertainty [9]. Research & Development (R&D) decisions touch each barrier.

Reach out to discuss this topic in depth.

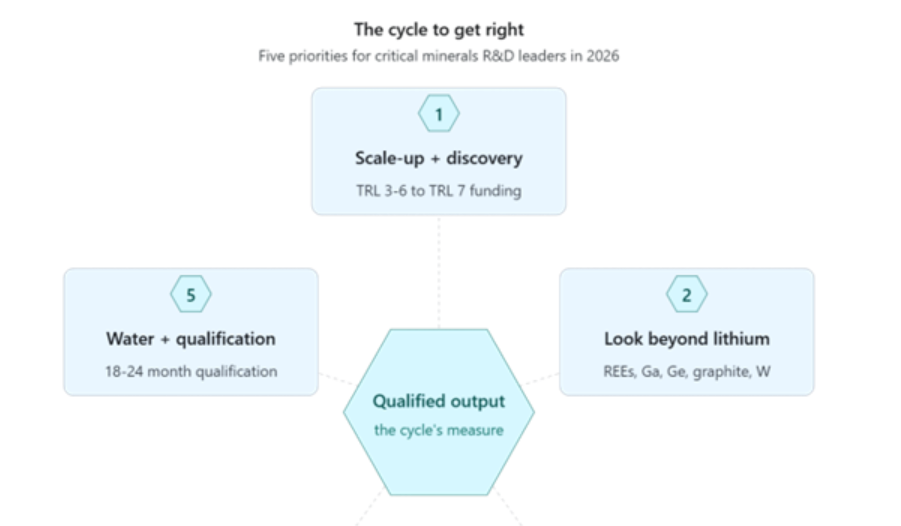

Priority 1: Resource scale-up alongside discovery

Basic science remains the foundation, but pilot and demonstration work is structurally underfunded relative to discovery. The April 2026 Department of Energy (DOE) Critical Minerals and Materials Accelerator is the diagnostic: Phase 1 advances awardees from Technology Readiness Level (TRL) 3 to 6, Phase 2 to TRL 7 [10]. The April 2026 Critical Minerals North America conference convened over 300 executives around strategies to approach midstream capacity [11]. Independently, Ucore Rare Metals’ RapidSX runs column-based solvent extraction three times faster than conventional mixer-settlers through engineering of proven chemistry [12].

Priority 2: Look beyond lithium

The investor narrative pulled R&D toward lithium for five years; the 2026 price action shows the bottleneck has moved. Rare earths, gallium, germanium, graphite, and tungsten absorbed the export-control rounds; lithium did not. The DOE Accelerator’s Topic Area 2 funds gallium, germanium, and silicon carbide processing, signaling the semiconductor-feedstock gap deserves attention alongside battery materials [10]. Portfolios benefit from weighting by application criticality: gallium and germanium feed semiconductors and fiber optics; antimony, munitions; tungsten, cutting tools and specialty alloys. The US’ import dependency on rare earth elements remains above 80%, with the European Union, Japan, and Korea facing comparable concentrations [13].

Priority 3: Build integration capacity alongside novel chemistry

Two R&D patterns coexist. Novel chemistry is well-resourced in US, EU, Australian, and Japanese labs. Flowsheet integration is what Chinese refiners spent two decades developing: solvent extraction circuit engineering, mixer-settler design, automation, and process control on stable chemistry, producing the lowest cost per tonne of separated oxide globally. Solvent extraction remains the only technology at industrial scale for global magnet demand [14]. Chinese refiners reached the cost-curve bottom through hundreds of small wins; comparable capability requires deliberate, sustained investment.

Priority 4: Valorize tailings and end-of-life products

Secondary recovery is where productivity-and-environment math works: recycling and tailings reprocessing expand processing depth on already-disturbed land, reducing the pressure on new mines in water-stressed regions.

About 8,500 global tailings facilities hold decades worth of material, at grades earlier processing left behind [15]. Idaho National Laboratory’s April 2026 assessment confirmed recoverable content across copper-gold porphyry, gold, lead-zinc, uranium, and phosphate tailings [15]. Peer-reviewed work demonstrates feasibility for lithium, nickel, cobalt, copper, rare earth elements, titanium, zirconium, and niobium recovery via hydrometallurgical leaching, mechanical activation, sensor-based sorting, and electrochemical recovery [16].

ReElement Technologies runs an ion-exchange platform for rare earth magnet scrap and lithium-ion battery black mass [12]; the DOE backed a US$475 million loan to Glencore Battery Recycling, plus Syrah’s Vidalia graphite facility and Novonix’s Project Kathari [5]. A tonne from these streams qualifies into the same supply chain as virgin concentrate.

Priority 5: Engineer for water stewardship and qualification velocity

Permitting, water management, and customer qualification are design problems R&D can shape directly. Flash heating, modular ion-exchange, and closed-loop solvent extraction reduce or eliminate effluent, making projects permittable where conventional processing would fail [12].

Closed-loop water reuse and genuine partnership with Indigenous and local communities deserve R&D funding alongside recovery. Discovery-to-first-production averages 16 years in the US versus 7-10 in Australia and Canada [17]. Customers in magnet, battery, and semiconductor industries take 18-24 months to qualify a new feedstock: magnet makers need rare earth oxide purity and dysprosium loading; battery cells need lithium hydroxide impurity profiles; semiconductor foundries need electronic-grade gallium and germanium. Co-developing specifications from the first pilot produces revenue years earlier.

A cycle worth getting right

The position a critical minerals company holds in 2030 is being set inside R&D portfolios in 2026 (Exhibit 1). Reserves attract attention; recovery decides what reaches a customer. Most minerals R&D is organized by mineral or site; the work benefits from cross-mineral teams by chain step. The cycle ahead is productive enough to close the supply gap, durable enough to scale, environmentally and socially sound enough to keep its operating license, and credible enough with communities and customers to last beyond the next price correction.

Exhibit 1: Five priorities for critical minerals R&D leaders in 2026.

If you enjoyed this blog, check out, Unlocking value through R&D process transformation in the age of AI – Everest Group Research Portal, which delves deeper into another topic relating to R&D.

If you’d like to continue this discussion, please contact Cecilia Van Cauwenberghe ([email protected]).

References

- Fastmarkets, Tungsten 2026: Geopolitics Sets Global Tone, Mar 2026. https://www.fastmarkets.com/insights/tungsten-2026-geopolitics-sets-global-tone/

- Benchmark Mineral Intelligence, Rare Earths Q1 2026 Price Review. https://source.benchmarkminerals.com/article/tight-supply-and-chinese-policy-drive-prices-rare-earths-q1-2026-price-review

- Interesting Engineering, Critical Minerals and Rare Earth Supply, Mar 2026. https://interestingengineering.com/research/critical-minerals-and-rare-earth-supply

- IEA, Global Critical Minerals Outlook 2025. https://www.iea.org/reports/global-critical-minerals-outlook-2025/executive-summary

- US Department of State, 2026 Critical Minerals Ministerial, Feb 2026. https://www.state.gov/releases/office-of-the-spokesperson/2026/02/2026-critical-minerals-ministerial

- DFC, Landmark Critical Minerals Investments, Feb 2026. https://www.dfc.gov/media/press-releases/dfc-highlights-landmark-critical-minerals-investments-strengthen-us-national

- Mayer Brown, US Government Equity Investments in Critical Minerals, Apr 2026. https://www.mayerbrown.com/en/insights/publications/2026/04/us-government-equity-and-equity-linked-investments-in-critical-minerals

- Natural Resources Canada, 30 Partnerships, $12.1B Capital, Mar 2026. https://www.canada.ca/en/natural-resources-canada/news/2026/03/canada-secures-30-new-critical-minerals-partnerships-and-unlocks-121-billion-in-mining-project-capital.html

- WEF and Columbia SIPA, Critical Minerals Need More Than Capital, May 2026. https://www.weforum.org/stories/2026/05/critical-minerals-targeted-derisking/

- Holland & Knight, DOE Critical Minerals and Materials Accelerator, Apr 2026. https://www.hklaw.com/en/insights/publications/2026/04/energy-department-releases-critical-minerals-and-materials-accelerator

- Critical Minerals North America Conference, Apr 2026. https://www.criticalmineralsnorthamerica.com

- RBC, Critical Minerals Processing, Apr 2026. https://www.rbc.com/en/thought-leadership/explained/critical-minerals-processing-the-wests-refining-challenge-and-the-technologies-closing-the-gap-2/

- USGS, Final 2025 List of Critical Minerals, Nov 2025. https://www.usgs.gov/news/science-snippet/interior-department-releases-final-2025-list-critical-minerals

- Rare Earth Mining, Top 10 Rare Earth Separation Technologies, 2026. https://rare-earth-mining.com/top-10-rare-earth-separation-technologies/

- Idaho National Laboratory, Critical-Minerals Recovery from Mine Tailings, Apr 2026. https://inl.gov/content/uploads/2026/04/INL-RPT-25-89279.pdf

- Springer, Recovery of Critical Metals from Tailings, 2025. https://link.springer.com/article/10.1007/s40831-025-01126-y

- Sustainability Atlas, Critical Minerals Supply Chains 2026, Mar 2026. https://sustainableatlas.org/post/trend-watch-critical-minerals-supply-chains-lithium-cobalt-rare-earths-in-2026-s-3085